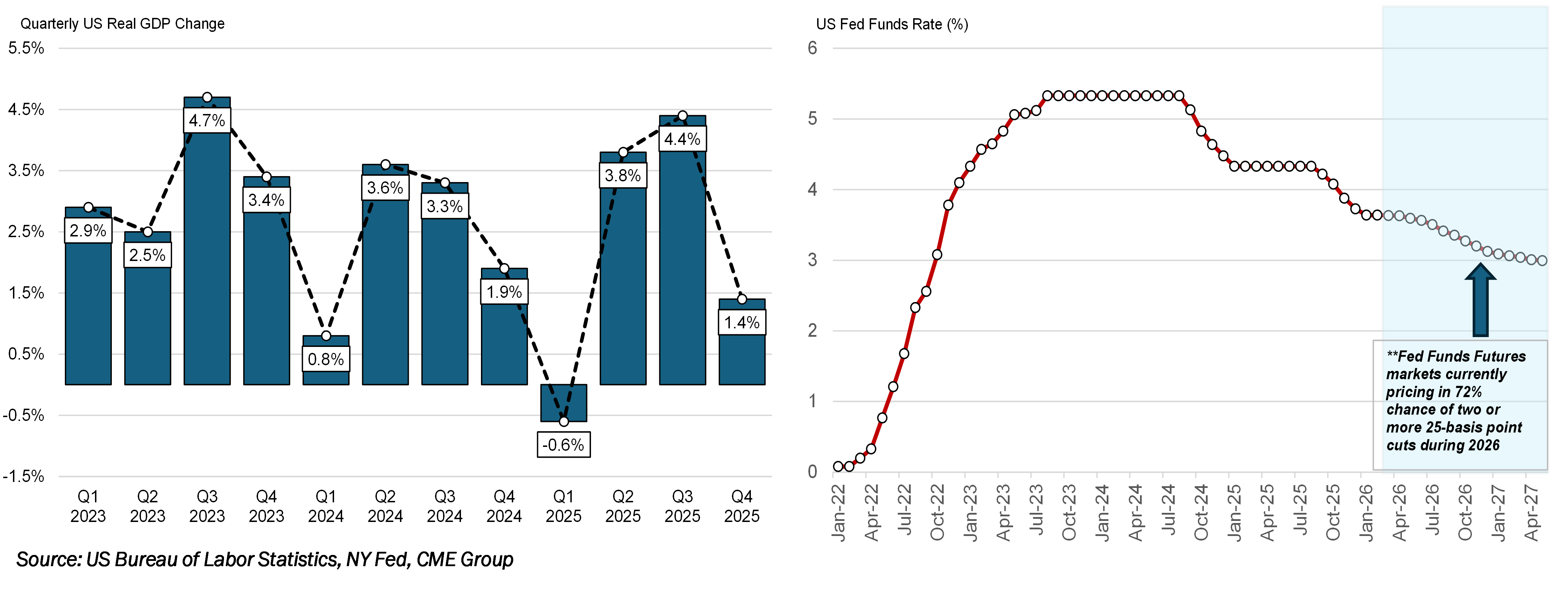

On January 30th, President Trump nominated Kevin Warsh to become the next Fed chair, replacing Jerome Powell when the latter’s term ends in May 2026. Warsh was a Fed governor from 2006 to 2011 and was known to favor holding rates higher for longer, particularly in the years after the global financial crisis. However, recent comments from Warsh suggest a more dovish stance (preference for lower interest rates), in line with the administration’s monetary policy preferences. Currently, the Fed Fund futures market is pricing in approximately 72% chance of at least two interest rate cuts during 2026, with negative implications for US dollar strength. The resilient economic activity in emerging markets – supported by a weaker US dollar – should underpin the back end of the crude pricing curve, while the expanding global crude balance in 2026 is expected to weigh on the front end of the curve. The growing oil demand and insufficient upstream investment at current price levels are expected to reinforce support for forward-dated pricing. As markets increasingly recognize the risk of future supply inadequacy, the crude forward curve has effectively shifted since Q4 2025 from backwardation to demand-driven contango (with future deliveries priced above spot).

The US Supreme Court ruled on February 20 against the validity of President Trump’s tariffs. In response, the Trump administration imposed a blanket global tariff of 10% and is reportedly working to raise it to 15% via a separate order, according to NBC. As expected, the ruling is likely to entangle the administration in a complex legal battle with numerous companies seeking refunds on approximately $175 billion in tariff revenue collected in 2025. Based on precedent, we expect the refund process will become protracted and highly contentious, as the administration is likely to challenge the ruling aggressively and delay, or potentially disregard, adverse tariff decisions. There is concern that Trump’s protectionist trade policies could represent a larger-than-expected drag on activity, ultimately pressuring the consumer and GDP growth in the coming quarters.