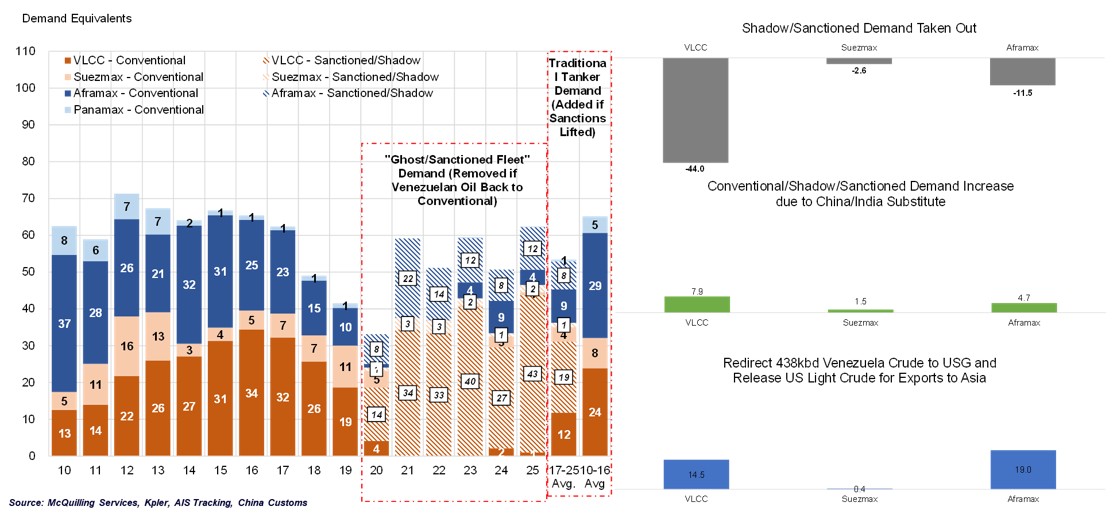

Since the first round of enhanced US sanctions in 2017, Venezuelan oil exports have steadily declined, with corresponding reductions in conventional tanker demand. Following 2020, a significant portion of tanker activity shifted to sanctioned and shadow vessels. With limited buyers, Venezuela crude has been directed to Southeast Asia via unconventional VLCCs before onward delivery to Northern China. The red dotted line the first graph highlights this shift, showing average tanker demand from 2017‑2025 on the left and 2010‑2016 on the right, underscoring the stark contrast in demand patterns before and after sanctions. Looking ahead, we anticipate a gradual recovery in tanker activity as new investments flow into Venezuela’s oil sector, with long-term tanker demand trending back toward pre‑sanction levels observed in 2010‑2016.

Since heightened US enforcement against Venezuelan oil flows began in December 2025, China has been forced to replace roughly 438,000 b/d of Venezuelan heavy crude feedstock with imports from the Middle East and West Coast Canada. This shift, in theory, supports conventional VLCC demand by roughly 7.9 vessel demand equivalent; however, the anticipated upside was delayed as refiners prioritize drawing down inventories of discounted Russian crude currently floating at sea due to recent enforcement actions, which could release tonnage previously acting as floating storage back into the trading fleet and temporarily pressuring freight rates. We expect the displaced 438,000 b/d of Venezuelan heavy exports, including cargoes aboard seized tankers, to be absorbed almost immediately by US Gulf refineries, well ahead of any new capital investment in Venezuela’s oil infrastructure. These volumes are likely to be carried primarily by Aframaxes, boosting regional demand by approximately 19.3 vessel demand equivalent as US refiners optimize heavy sour crude runs. Elevated Venezuelan heavy sour imports could displace US‑produced light grades from domestic refinery slates, freeing these barrels for export to Asia and potentially supporting a net of 14.5 VLCC vessel demand equivalent.