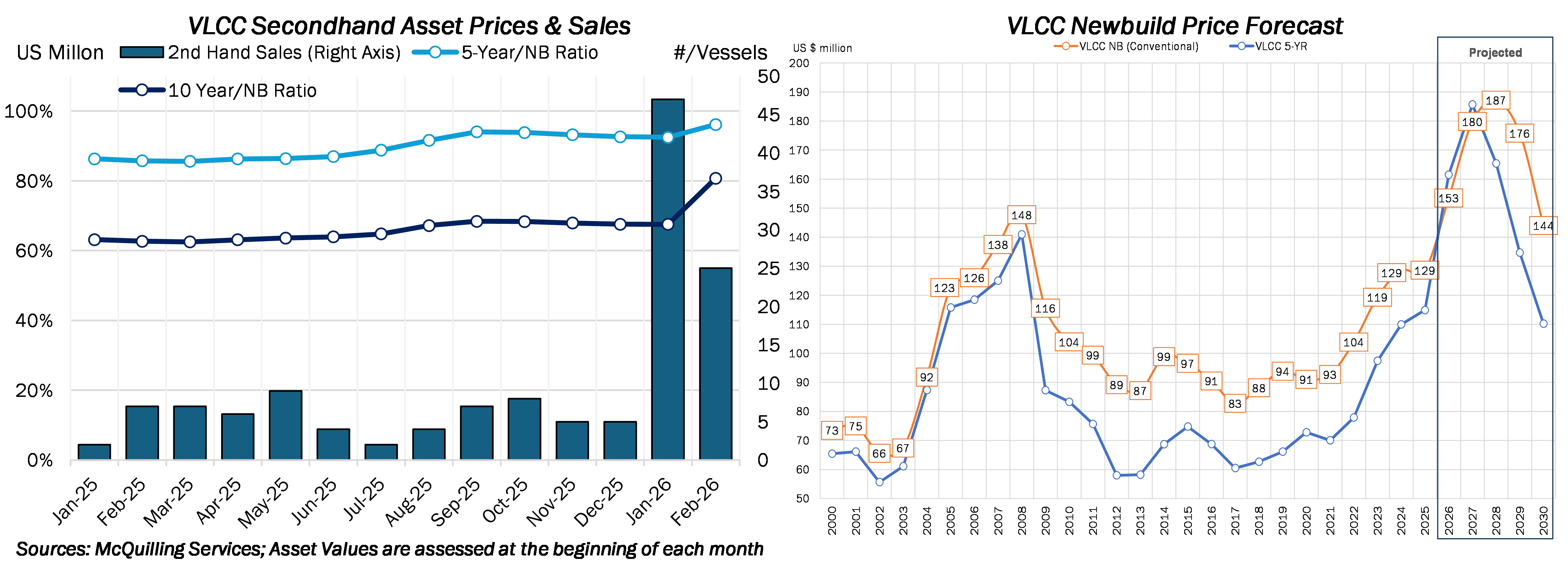

Our assessments of tanker asset values, particularly for secondhand VLCCs, have surged since the beginning of the year. Ownership restructuring within the conventional fleet appears to be the primary catalyst, as MSC-backed Sinokor has reportedly acquired at least 52 VLCCs via secondhand transactions since January, accounting for approximately 73% of all recorded deals over this period (bars in the left graph). This highly concentrated buying activity has triggered a rapid repricing of secondhand assets, with 5- and 10-year-old VLCC value assessments increasing by US $4.5 million and US $17 million, respectively, within a single month – marking the largest one-month increase in secondhand VLCC prices over the past 25 years. When asset values are expressed as a ratio to newbuilding prices (lines in the left graph), the magnitude of this move becomes even more pronounced as VLCC newbuilding prices remained firm at around US $130 million (basis Korean/Japanese yards) over the same period. This divergence underscores buyers’ strong preference for prompt tonnage delivery to capitalize on the current phase of exceptionally firm tanker earnings. The recent surge in asset values should not come as a surprise to our premium clients.

As outlined in our 2026-2030 Tanker Market Outlook, we anticipated that secondhand VLCC prices would outperform newbuilding prices in 2026-2027, underpinned by our conviction in a sustained period of firm spot earnings. In the meantime, shipyards in Northeast Asia are facing prolonged orderbook turnover due to reduced productivity, an aging workforce, and broader demographic challenges. Policy uncertainty has also emerged as a key risk factor, including the USTR’s Section 301 and the latest Maritime Action Plan, and the postponement of the IMO Net-Zero Framework vote. As global merchant fleets built during the 2005-2012 single-hull phaseout era gradually age out, ordering new oil tankers will face intensifying competition from LNG projects, mega-container orders, and an eventual dry bulk replenishment cycle, all of which are rapidly tightening global shipyard capacity. This, combined with our view of rising commodity prices (oil, steel) and a weakening US dollar, points to further increases in newbuilding contract prices. We expect VLCC newbuilding prices to rise to US $187 million by 2028, still below the inflation-adjusted peak observed in 2007–2008.