US OFAC surprised the market on Oct 22nd by sanctioning Russia’s two largest oil companies – Rosneft and Lukoil, and their subsidiaries, seeking for an immediate ceasefire. According to the press release, the wind down period will end on November 21st, 2025, giving importers a very short window to substitute these volumes. Following the latest sanctions, India’s oil majors officially announced adapting the refinery operations to meet the compliance requirements; China’s state-owned refiners will also reportedly cut imports, although the majority (80%+) of Russian crude to China is utilized at independent refineries.

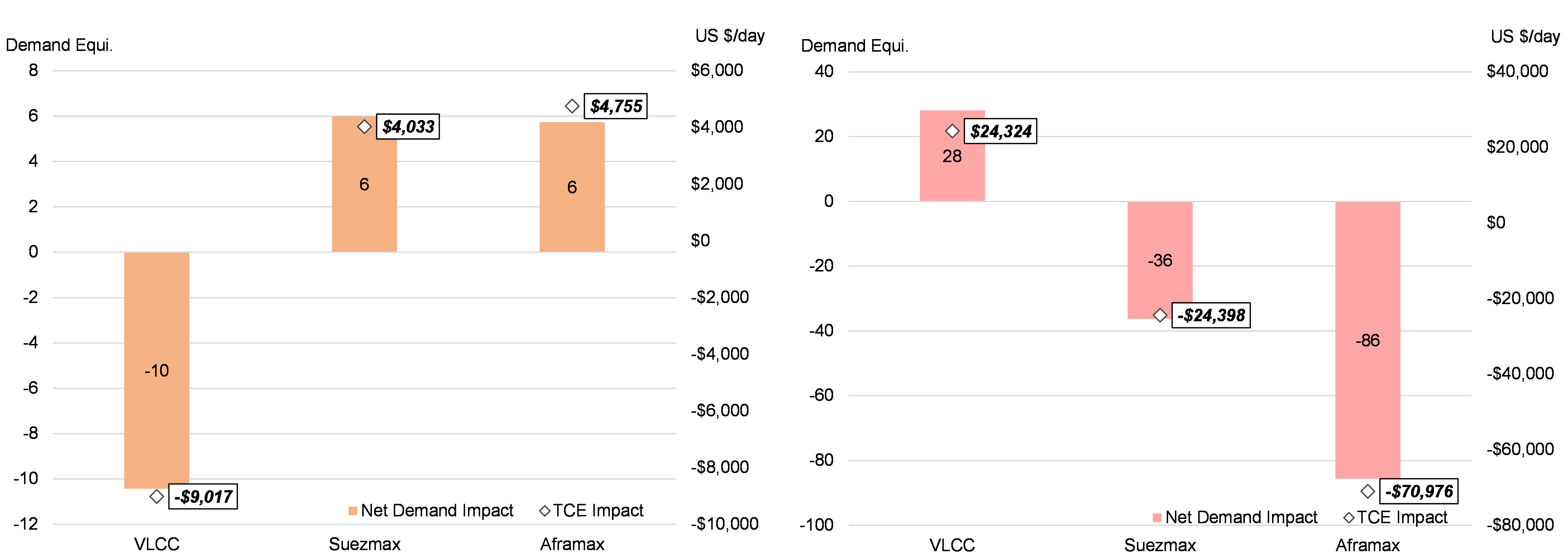

Despite lowered Suezmax and Aframax demand for Russian exports, we foresee overall conventional mid-sized demand and earnings benefiting from the recent developments, as charterers try to avoid paying escalated VLCC freight and instead use mid-sized tankers when possible. Prior to the US sanctions and given 40% of Russian>India crude flows on term contracts, we anticipated Reliance would designate one of the two mega refineries in Jamnagar (660,000 b/d) to process non-Russian crude for exports to Europe in order to comply with EU’s 19th sanctions; however, this scenario is no longer on the table. Assuming India fully cuts Russian crude imports with 75% of this volume picked up by China, our demand equivalent calculations return a net negative for VLCC, as part of long-haul VLCC demand for Middle East+Atlantic>China will be replaced by shorter-haul flows to India. Demand for mid-sized tankers, on the other hand, could find significant support as Russian crude from Western ports could sail further distances to the Far East, ironically forming the sanctioned oil flows by sanctioned ships to sanctioned ports and refineries. This impact starts to unwind and potentially revert as we gradually reduce China’s intake of Russian crude. In the event of closed arb and/or geopolitical measures (including China cutting imports from Russia following a US-China trade deal), VLCC demand will inversely benefit (right chart) by US $24,324/day while earnings of mid-sized tankers to drastically retreat. There are two major crude pipelines between Russia and China (Skovorodino-Mohe and Atasu-Alashankou, totaling 800,000 b/d) and are reportedly running close to full capacity.

Fig. 1: If India Cuts 100% of Imports from Russia and China Picks Up 75% Fig. 2: If India Cuts 100% and China Cuts 50% of Seaborne Imports

Source: McQuilling Services, AIS Tracking