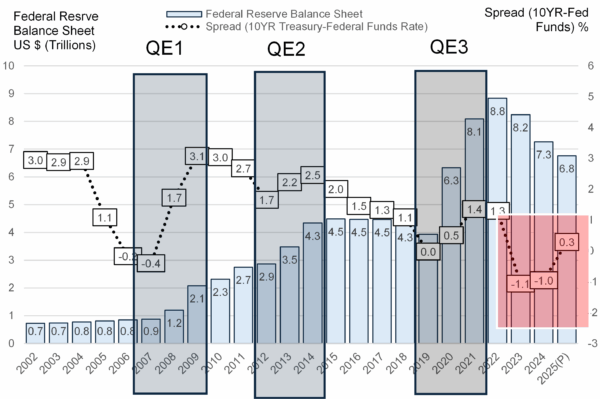

The macroeconomic environment is an important factor in the outlook for tankers. OPEC+ knows that a weaker US $ will promote both 1) more Asian demand for oil (due to lower local currency pricing) offsetting weaker Western demand, with a contango structure; and 2) incentivizing re-stocking initially as lagging stimulus impacts in the West leads to global economic growth in 2026/27. A US interest rate cut paired with a Japanese rate increase would result in a weaker US $ and slower demand. Weaker demand and limited ability for supply side adjustments could result in relatively weaker front-end prices while a weaker US $ and economic stimulus release (pending monetary stimulus) would support forward prices. Ultimately, a weakening US $ cycle would stimulate emerging market demand for commodities (initially to restock), leading to increased utilization for tankers. Furthermore, we note that OPEC+ may be “front-running” supply increases (eerily similar to 2003) in anticipation of this macro development. Our read of this situation suggests they are positioning for “back-end” curve control once emerging market demand increases (weaker US $), with limited spare capacity available to meet this demand (see 2004-2008 commodity cycle).

As a result, we foresee a strong and cyclical crude tanker market moving into Q4 2025 and 2026, supported by elevated tanker demand (OPEC+ supply increase amid weakening US dollar and crude contango pricing) and a shrinking supply equivalent of the crude tanker fleet. With 4 consecutive years of low VLCC newbuilding deliveries and high deletions from the conventional fleet amid age limitation and sanctions, the VLCC supply equivalent is projected to shrink by 4.7% in 2025 and another 1.3% in 2026, while demand in 2026 is projected to approach 10% y-o-y.

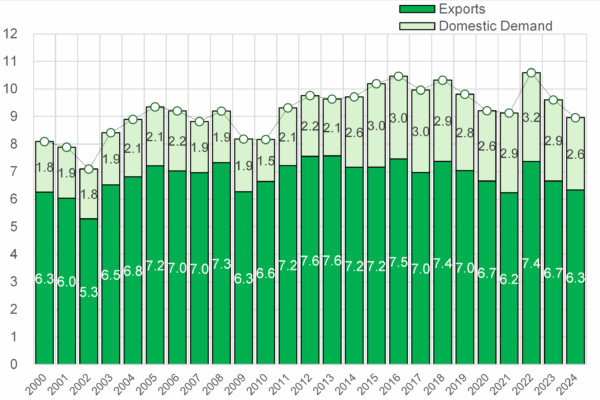

Fig. 1: Fed Balance Sheet vs. 10-Year Treasury Fig. 2: Saudi Demand and Export Figures

Source: OPEC, Kpler, McQuilling Services