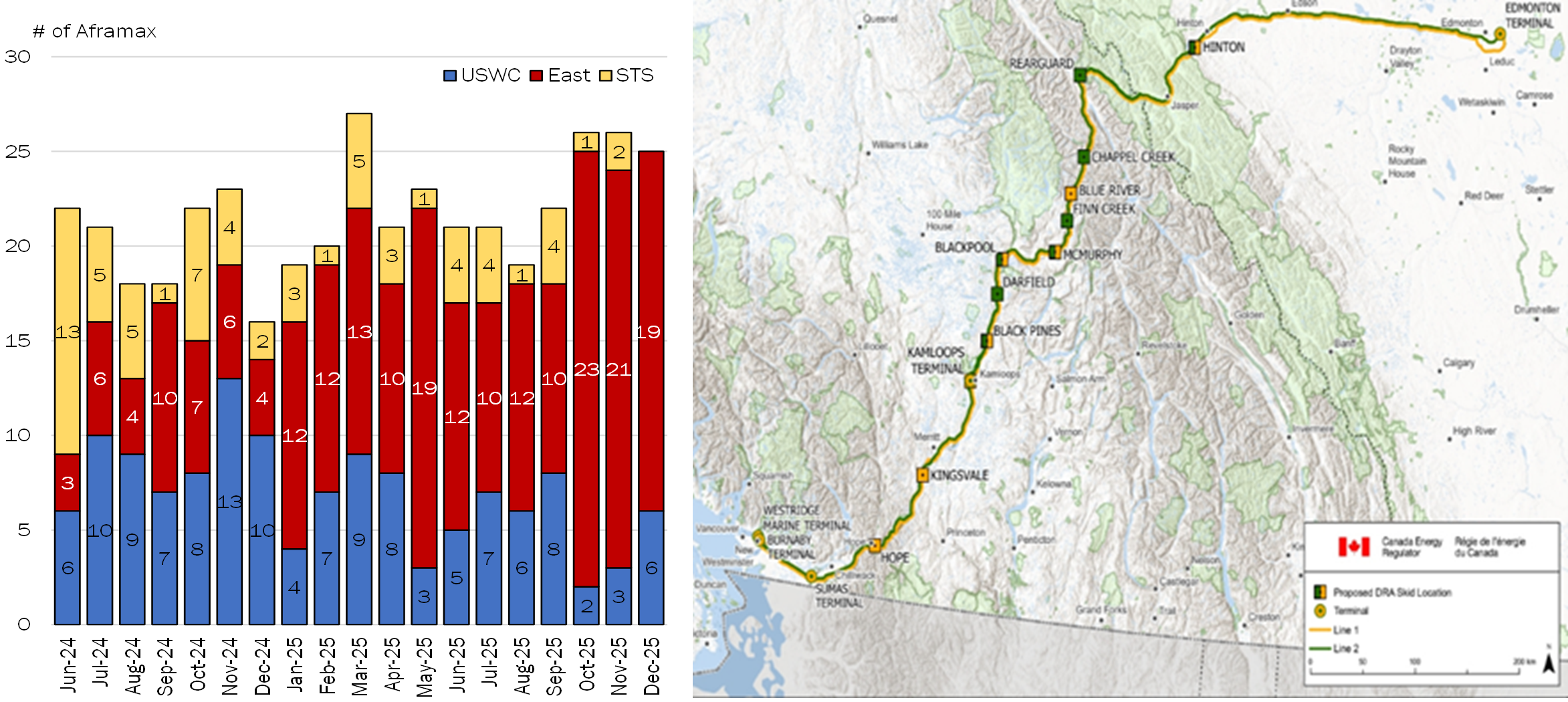

In 2026, the key drivers for the Trans Mountain pipeline system, including the TMX expansion, which has tripled export capacity from the Port of Vancouver to approximately 890,000 b/d, will primarily hinge on three factors: (1) operational utilization and ramp-up, (2) the removal of port-side bottlenecks that determine the number of tankers able to load, and (3) regulatory and toll certainty, which influences shipper nomination behavior. On utilization, TMX’s January 2026 capacity update indicates that system nominations were not apportioned for the month, suggesting that chartering demand did not exceed available capacity. This points to a transition from an oversubscribed bottleneck environment toward a more balanced capacity regime.

However, increased TMX throughput is only part of the support for Aframax demand at Vancouver, while the key resides in higher volume for long-haul Asia-bound. About 82% of Q4 2025 Aframax liftings have discharged in China or other Asian countries, while only 14% ended up in the US West Coast refineries during the quarter. The trend is expected to continue into 2026 as the TMX crude serves to replace heavy Venezuelan barrels that will now be largely routed to the US Gulf. Vancouver exports via ship-to-ship lightening have also remained low, given the rising VLCC freight rates and the lack of naturally positioned tonnage in the region. That matters for exports because less apportionment generally means shippers can plan steadier month-to-month line space, which supports more consistent marine loading programs out of the Vancouver area rather than opportunistic fixtures.