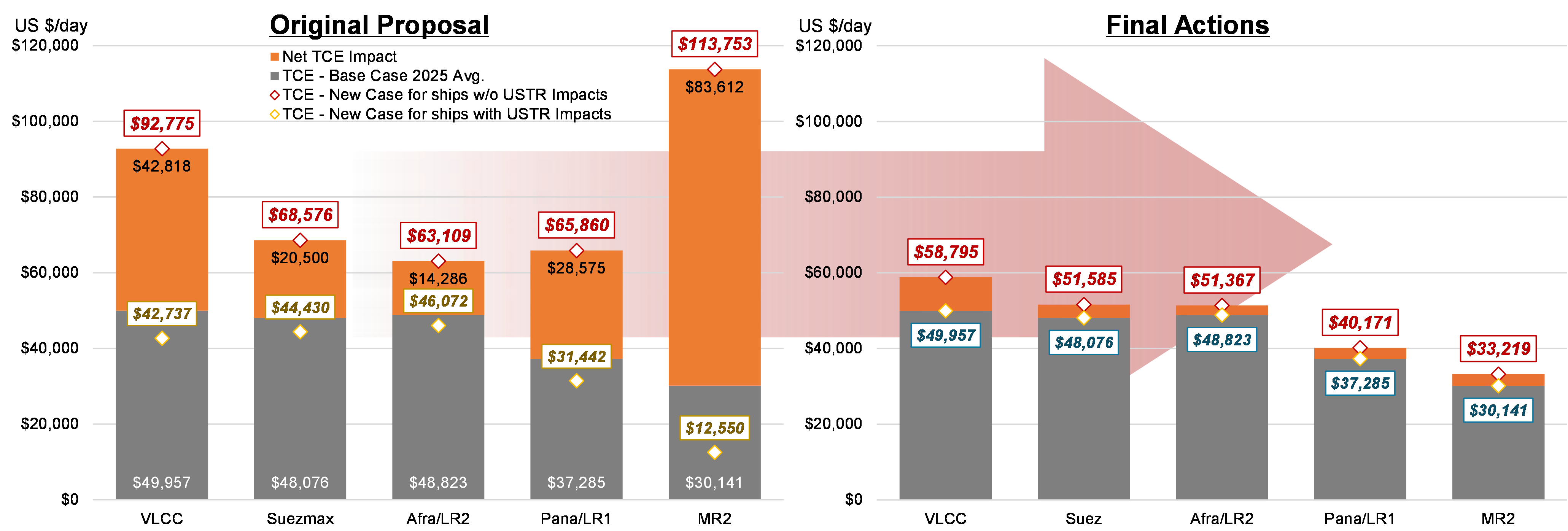

To measure the impact of the USTR’s proposal on TCEs, we have categorized each AIS-derived voyage for US imports and exports since 2023 based on the owner, operator and build yard, as well as their exposures on increased port costs based on net tonnage and applicable exemptions. We assume these affected tankers will be substituted by non-Chinese built ships but only those that have traded in the Americas market since 2023. Taking the Panamax/LR1 trading fleet as an example, of the 204 vessels that are not Chinese built or owned, there are 65 ships that have been exclusively deployed in the East of Suez or European market, and thus less likely to reposition for US-related trades. Based on the adjusted demand/supply fundamentals and fleet utilization%, we foresee a two-tier market will be created; tonnage without USTR impact could earn US $2,500-8,800/day higher across the five sectors (right chart), since rate premiums are needed to incentivize owners to shuffle these ships to trades including Middle East>USG+USWC (VLCCs), Latam>USG+USWC (mid-sized), Africa+Europe>USAC (mid-sized and Chinese-owned MR2s). The TCE impact has been notably tempered from the original proposal (left chart) where no exemptions were provided.

Of these impacted routes, the VLCC Middle East>USWC trade caught our attention as over a quarter of the demand is filled by Chinese owned tonnage after lifting Colombian, Guyanese and US crude at PTP (West Coast Panama) to the East. Chinese-owned VLCCs may adopt full STS lightering services to discharge in the PAL as a bypass; however, the elevated freight and risks on demurrage does not work out in owners’ favor and likely to further price out Middle Eastern crude in the USWC refiners to Canadian grades. Meanwhile, storage in Caribbean (located less than 2,000NM; i.e., Bahamas) could become very attractive for Brazilian and Middle Eastern crude and fuel oil before being re-exported to the US. While the USTR Section 301 actions will create chaos and fleet inefficiency for tankers, the final impact could be revised again after the talk between President Trump and President Xi.

Source: McQuilling Services, AIS Tracking