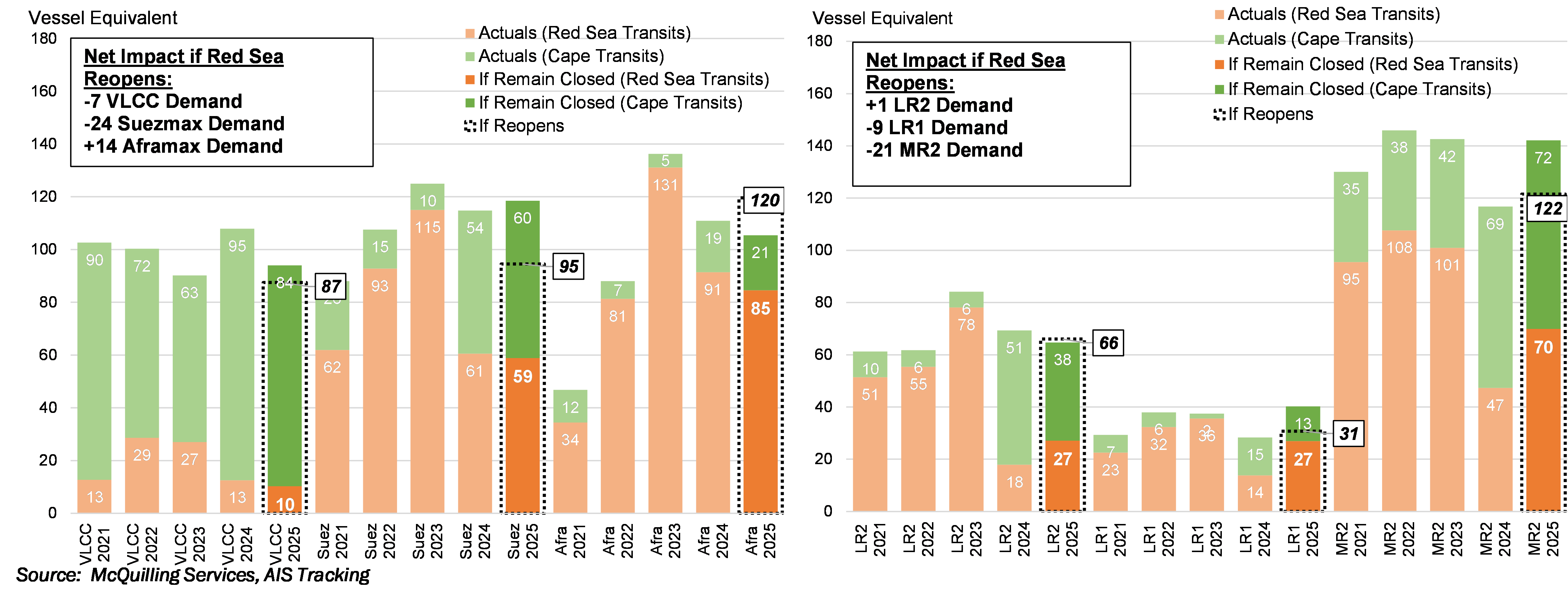

The change in trade flows and market fundamentals so far this year has caused us to revise our analysis for the tanker demand impact if the Red Sea chokepoint reopens during our forecasting period. Compared to a net reduction of 15 vessel equivalent estimated in the beginning of this year, the negative impact on VLCC demand is now only 7 ships, representing some upward revision of $6,900/day on earnings (1 VLCC = $865/day). The tempered impact is mainly attributed to this year’s lowered VLCC cannibalization of mid-sized tankers for both crude and refined product trades. Aframax tankers may find continued support, although this trend also highly depends on the future of Russian crude exports to India and China. Aframax demand could be pushed further if China takes additional Russian barrels from the Western ports while VLCCs will benefit the most if both China and India cut their imports.

On the refined product side, the net pull of LR2 demand estimated at the beginning of the year has now flipped to net push as the tight diesel balance in the Atlantic Basin could be eased significantly by imports from the East of Suez via LR2 tankers through the Red Sea. MR2 demand, on the other hand, may see deeper pressure (-21 equivalent or -$9,000/day) after the return of EoS cargoes. Refining margins on East and West Coasts of the Atlantic Basin are expected to fall significantly from the current heights, as well as MR2 demand in the region. Part of the cargo flows from the East (namely India) may also push out USG products in LATAM countries where importers are actively seeking to substitute Russian oils for blending purposes and retail sales.