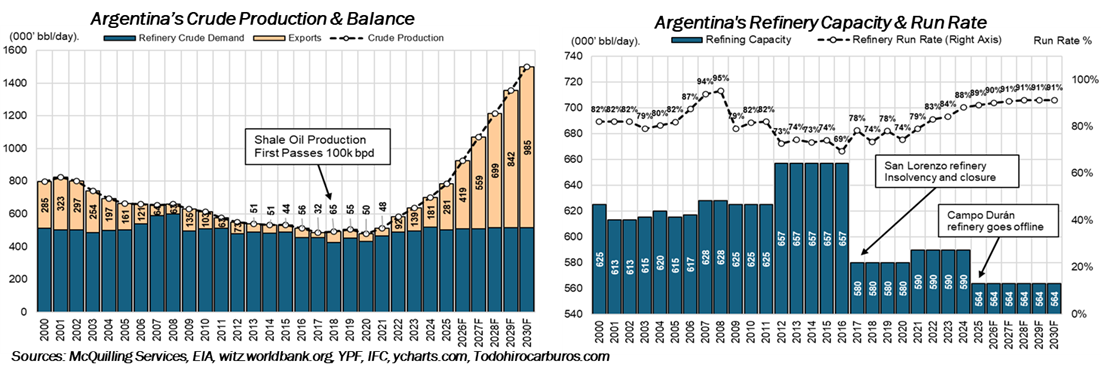

Until recently, Argentina’s crude oil production peaked in May 1998 with an average of 859,000 b/d driven by conventional drilling. Production had been on a steady decline until 2018, when shale oil production first surpassed 100,000 b/d, creating the first sign of Argentina’s crude oil boom. This continued into 2019 but was quickly reversed due to the oil demand crash caused by Covid-19 lockdowns. Since then, conventional oil has continued to dwindle to only 210,000 b/d in 2025, with a reversed trend coming from shale oil production in Vaca Muerta (“Dead Cow” in English). Through a series of debottlenecking projects on midstream, Argentina is projected to produce around 1.5 million b/d by 2030, according to YPF – the largest and state-owned integrated energy company in the country. This growth in production is supported by the recent Trans-Andean pipeline reactivation and the Oldelval pipeline upgrades, which direct crude to the newly expanded Suezmax terminals in Puerto Rosales. Current pipeline capacity now sits at 750,000 b/d with export capacity around 540,000 b/d. The export capacity could see a further jump when the VMOS pipeline and Punta Colorada VLCC terminal both set to begin operations in late 2026 – this new pipeline and terminal capacity will start at 180,000 b/d before ramping up to over 700,000 b/d in 2028. By then, Vaca Muerta production will reach 1.5 million bpd with an available export level close to 1.0 million b/d.

While crude production looks strong, minimal changes are expected on Argentina’s refining capacity. With only 3 confirmed upgrades aimed to improve run rate and refinery capabilities, average run% n is set to inch up by only 2% over the next 5 years; there is also no current plan to build new refineries. Meanwhile, the Campo Duran Refinery (26,000 b/d) went offline at the beginning of this year due to an acquisition by YPF, now focusing the refinery to rely on natural gas instead of crude oil as feedstock. With inflation massively retreating from 200% in 2023, Argentina’s GDP is on trend to further grow by 3% in 2026, supporting demand for refined oil products. As the capped refining capacity only meets ~80% of domestic oil demand, Argentina has been a net importer in the CPP market while merely importing crude oil. It’s also not unreasonable to see renewed interest in raising domestic refining capacity, although these projects usually take years to develop. Detailed analysis on Argentina’s oil fundamentals and its impact on the oil tanker market will be shared in the 2026-2030 TMO.