Since beginning to track switchovers 5 years ago, the LR2 switchover has been cemented as a tanker market function, no longer merely a trend. Since Q3 2024 as Ukraine drone attacks heavily disrupted Russian’s oil product balances and available CPP exports, CPP tanker earnings took a deep dive after Russia announced oil product export bans on key products including gasoline and naphtha. Earnings for dirty-Aframaxes, on the other hand, continued to find upside support as Russia instead exported crude, and Canada’s TMX pipeline throughput kept ramping up. The widening gap of the earnings structure, coupled with a drastic influx of LR2 newbuilds, have pushed a net of 15 and 31 LR2s to “dirty up” in 2H 2024 and 2025 through August. We anticipate the “clean-to-dirty” switchovers to continue in our forecasting period, considering 93% of the Aframax-sized tanker orderbook consists of coated LR2s and the crude tanker market is expected to be stronger than the CPP market, with the latter pressured by the heavy MR2 orderbook.

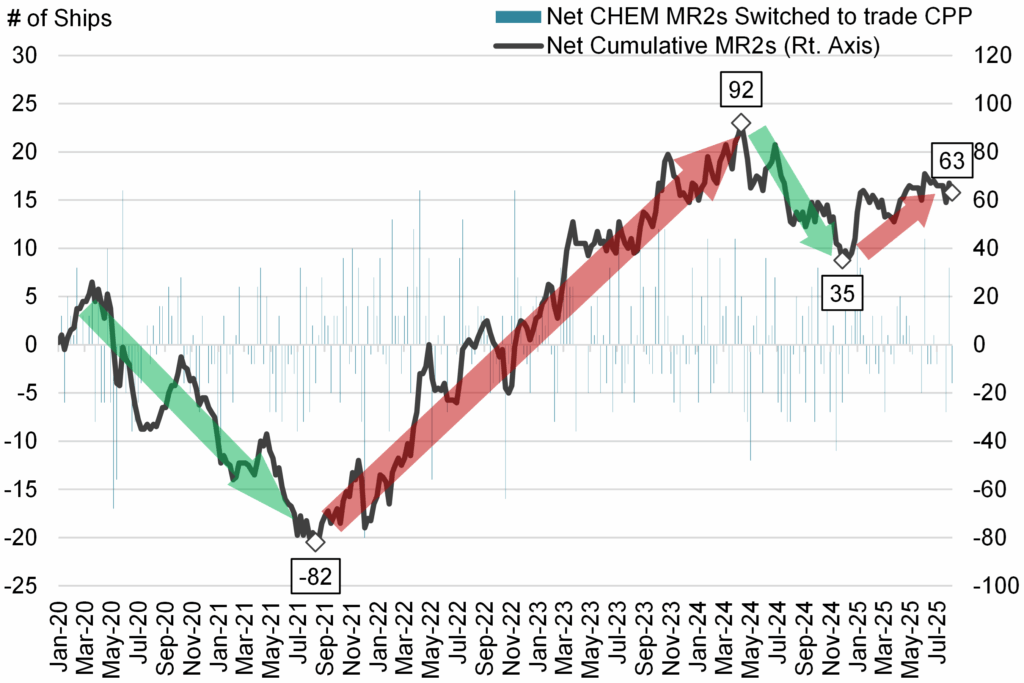

It is more challenging to track switchovers of chemical MR2s, as segregated cargo tanks allow them to carry various chemical and oil products at the same time. The cumulative MR2 switchovers to CPP trading (right graph) have shown notable patterns since 2020; more interestingly, these patterns correlate to the strength in earnings in either chemical or oil product markets in the East of Suez markets, but less so in the West. During the height of the COVID pandemic, when chemical tanker earnings were strongly supported by prolonged port turnovers in China, a net of 82 CPP-trading MR2s joined chemical trading; the trend flipped since Russia’s invasion of Ukraine, which drastically pushed oil tanker demand while chemical demand retreated amid recession. This incentivized a net of 170 chemical MR2s rejoining the CPP market. We foresee the chemical > CPP trend to continue moving forward, suggested by the massive orderbook for IMO2 MR and stainless steel-coated J19s, but also a series of new Para-xylene (PX) plants in China putting negative impact on chemical tanker ton-mile demand.

Fig. 1: LR2 Switchovers – Crude & Refined Products Fig. 2: MR2 Switchovers – Refined Products & Chemical Products

Source: McQuilling Services, S&P Global