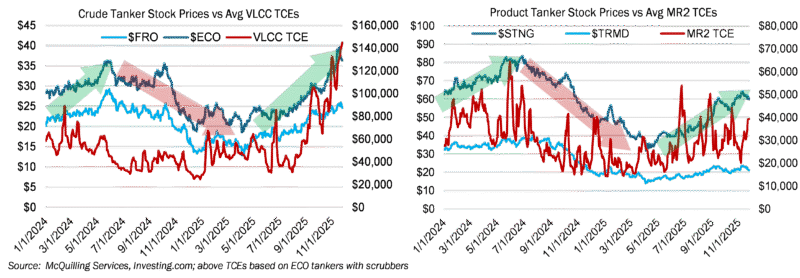

The oil tanker market is now back to the spotlight for investors following fundamental support from easing OPEC+ cuts and the geopolitical impact from USTR/China retaliation as well as a potential Russia/Ukraine peace deal. In addition to favorable dividends, investing in oil tanker stocks, especially those with heavily weighted VLCC fleets (left chart), have had impressive gains YTD2025. Stock prices such as Frontline Plc ($FRO) and Okeanis Eco Tankers ($ECO) gained 63.3% and 70.8%, respectively, since January, while the S&P 500 benchmark has registered gains of 15.3% (as of 11.25.2025). Interestingly, we have captured a strong correlation in the same period with over 70% R-squared between tanker earnings and stock prices, indicating significant interest from equity investors. Equity prices for product tanker owners have underperformed slightly relative to the crude tanker owners’ segment but are in line with the weaker CPP tanker earnings (red lines in charts below) pressured by the excessive supply-side pressure and soft end-user oil consumption.

The correlation between stock prices and tanker earnings varies among different shipowners, likely related to many other variables such as tanker fleet diversification (i.e. Scorpio announcing their reentry into VLCC owning), change in management structure, ship deployment between East and West of Suez markets, as well as timing when financial reports and earnings are released. Even though the correlation decreases marginally over a longer time horizon, we observe overall trendlines; in other words, elevated tanker earnings usually suggest higher stock prices and vice versa. This is evidenced by the downward correction in stock prices of product tanker owners between July 2024 and April 2025 when MR2 earnings coincidentally experienced counter-seasonal “winter markets” in 2024. As McQuilling forecasts continued bullish sentiment for crude and product tanker markets headed into 2026, this could provide upside support for shipping stock prices; however, one factor that shouldn’t be ignored is the narrowing margin for “carry trade”, which may suggest investments (including equity investment in the US-listed stocks) could see gradual outflows to the overseas markets.