The Federal Reserve embarked upon its rate cutting cycle on September 17th by cutting interest rates 25 basis points. Officials are navigating an economy reshaped by sweeping policy experiments. Trump has imposed tariffs that far exceed those of his first term, raising costs for manufacturers and small businesses. The full effects on consumer prices remain unclear as companies adjust supply chains and pricing strategies. Sharper curbs on immigration could be contributing to a slower pace of job gains by reducing labor force growth. Some policymakers have been more concerned about inflation, which has been running above the Fed’s target for more than four years. They worry that businesses and consumers could become more accustomed to price increases in ways that make inflation more persistent. They are also uneasy about making bolder commitments to lower rates at a time when stocks are hitting new records and new tax cuts might provide stimulus in the months ahead. Several of these officials acknowledge that tariffs may temporarily push up prices, but they warn that higher costs from imported goods and materials could sap hiring as firms shield profit margins from the hit delivered by tariffs. In addition, taxes on imports will deplete consumers’ purchasing power as firms pass along higher costs.

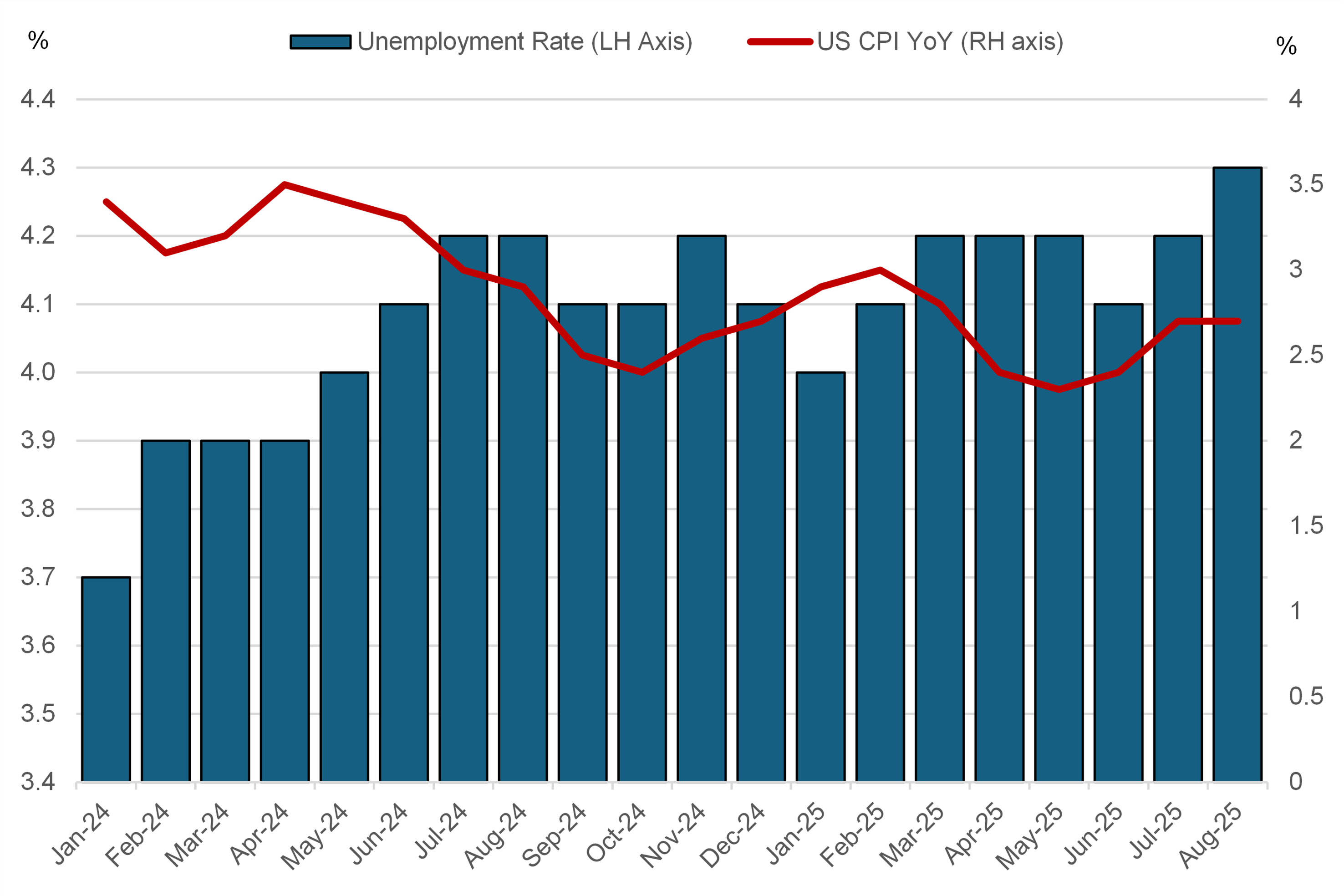

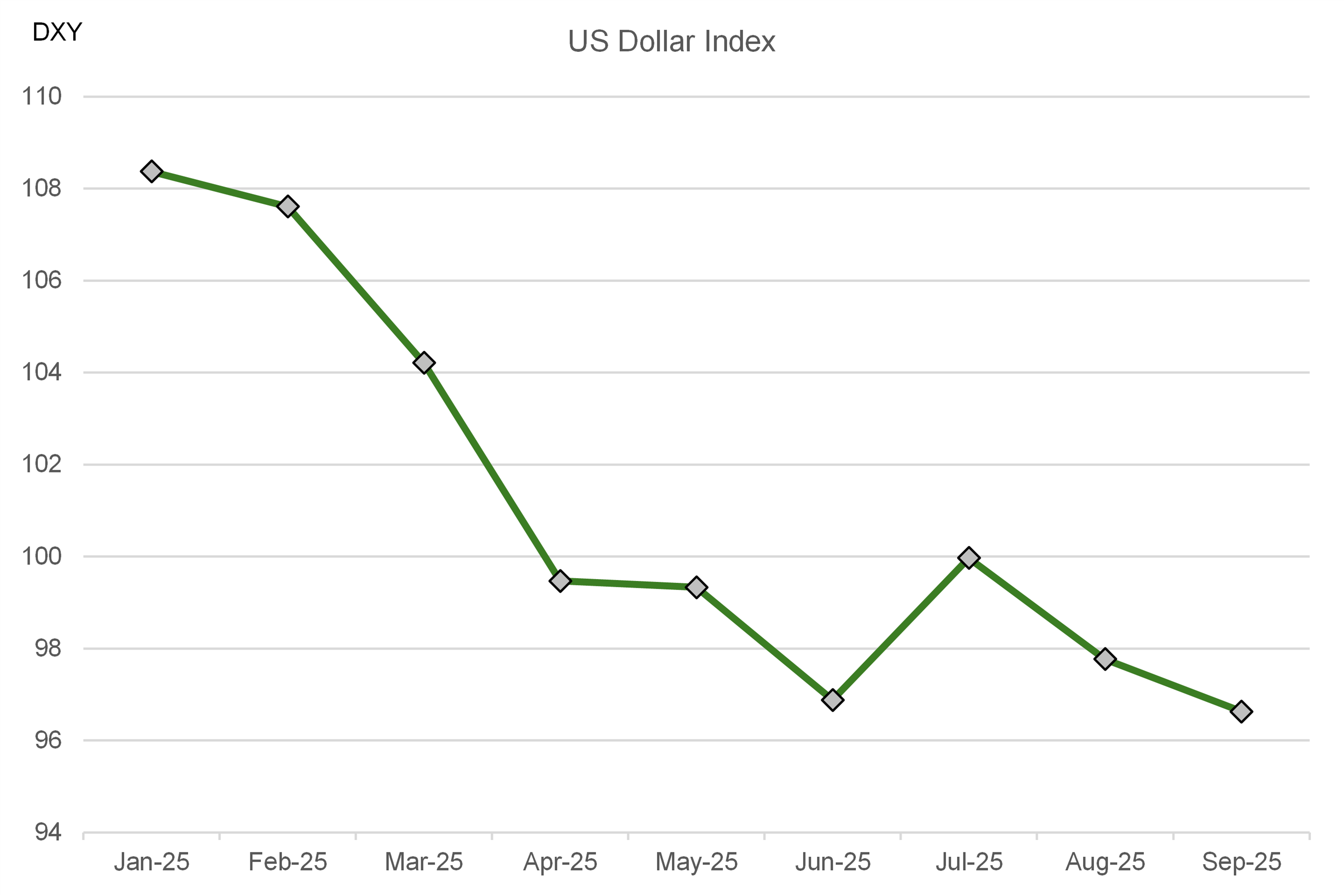

Fed officials have debated how to manage those tradeoffs all year long. In leading his colleagues to cut rates, Powell is making a calculation that the risks from inflation may be easier to manage and that the Fed should accept more inflation risk to prevent deeper cracks from imperiling the labor market. The left-hand graph shows how the US unemployment rate has been creeping up with inflation has eased somewhat but is still remaining above a level that policy makers are comfortable with. As a result of today’s Fed Rate decision, we continue to see downward pressure on the US Dollar (right-hand graph), precipitating one of the conditions necessary for continued OPEC+ production growth and emerging contango structure that would ultimately incentivize stronger VLCC activity ex-AG.

Fig. 1: US Unemployment Rate and Consumer Price Index Fig. 2: US Dollar Index

Source: US Bureau of Labor Statistics, Marketwatch