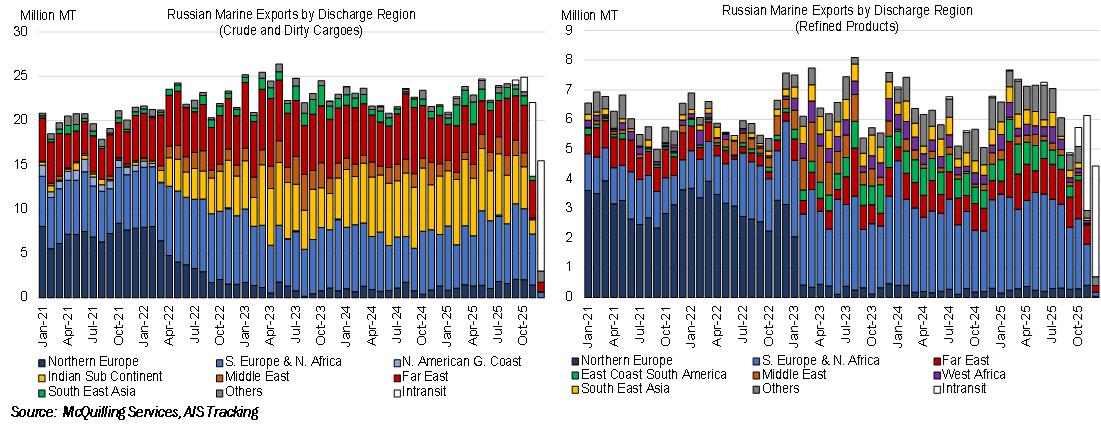

Despite the latest US penalties on Rosneft and Lukoil and sanctions imposed throughout the year, Russia remains deeply engaged in ongoing war with Ukraine as there has been limited progress toward a peace deal. According to our AIS tracking, Russia exported approximately 22.5 million ton of crude per month from Jan-Oct 2025, a 3.9% jump from the same period last year. Overall export, however, saw a notable drop in Nov-Dec 2025 following 1) India’s oil majors temporarily halt imports from Russia; 2) China’s major port group in Shandong (where most teapot refineries reside) blacklisted by the US; 3) Ukraine drone strike damaged and capped Russia’s export capacity from the CPC terminal in the Black Sea. The CPC terminal usually keeps 2 of the 3 SPMs operational for both Russian and Kazakhstan crude exports. The recent attacks have damaged SPM-2 while repairs and weather delays at SPM-3 have postponed the original restart date from Dec 15th to the end of year, leaving only SPM-1 operational at 800,000 b/d. As a result, we expect Russia to only export a monthly average of 15.5 million ton of crude in Nov-Dec – nearly 30% lower than last year – with Black Sea>India contributing the most decline in export volume.

On the CPP side, volume drops occurred earlier amid refinery offline and extended partial export bans on gasoline and diesel; a 24% decline in Russia’s oil product exports is captured in Aug-Dec compared to earlier months of 2025. Direct exports to Latam and Africa countries (green/light blue/purple bars in the right graph) retreated the most due to US/EU/UK blacklisting shadow ships exporting Russian oils above the Price Cap, which also explained the favorable refining margins and exports from the US Gulf and Mediterranean in 2H 2025 as importers substitute Russian barrels. The future of Russia oils remains uncertain at the time of writing. As noted in the November Short-term Forecaster, in the event sanctions were lifted on Russian oils and the Russian tanker fleet (Sovcomflot), McQuilling projects demand increases for up to 56 Aframax equivalent assuming 700,000 b/d of additional Russian crude exports to China and India, while a net of 23 Aframaxes (average age at 18yrs) may return to the conventional fleet. A more robust scenario analysis will be shared in the upcoming 2026-2030 Tanker Market Outlook (TMO).